How I Turned Cosmetic Surgery Costs into Tax Wins — A Smart Strategy

What if a life-changing procedure could also be a smart financial move? I never thought cosmetic surgery expenses could tie into tax planning — until I learned the rules. It’s not about vanity; it’s about strategy. With the right approach, medical costs can become deductions. This is how I navigated the system legally, saved money, and turned a personal decision into a smarter financial outcome. The journey began with a simple question: can something done for appearance ever count as a legitimate medical expense? The answer, as it turns out, lies in the details — and in understanding how the tax code defines necessity.

The Unexpected Link Between Medical Procedures and Taxes

At first glance, cosmetic surgery and tax deductions seem worlds apart. One is often viewed as a personal choice, the other as a matter of financial compliance. Yet under U.S. tax law, the line between aesthetic enhancement and necessary medical care is not always clear. The Internal Revenue Service (IRS) allows taxpayers to deduct qualified medical expenses that exceed 7.5% of their adjusted gross income (AGI), provided they are primarily aimed at alleviating or preventing a physical or mental health condition. This opens the door for certain procedures traditionally labeled as cosmetic to qualify for tax relief — but only when supported by medical justification.

Consider reconstructive surgery following trauma or illness. A woman who undergoes breast reconstruction after a mastectomy due to cancer may find that the procedure — while involving elements of cosmetic restoration — is fully deductible because it addresses a direct medical consequence of disease. Similarly, facial reconstruction after an accident, skin grafts following severe burns, or jaw realignment after an injury are all examples where form follows function, and the IRS recognizes them as medically necessary. In these cases, the goal is not simply to improve appearance but to restore physical integrity and psychological well-being.

The distinction hinges on intent and documentation. If a surgeon performs rhinoplasty solely to refine the shape of a nose for aesthetic reasons, it does not qualify. However, if the same surgery corrects a deviated septum that causes chronic sinus infections and breathing difficulties, it becomes a functional intervention — and therefore eligible for deduction. The IRS does not dismiss procedures based on appearance alone; it evaluates whether the primary purpose is therapeutic. This subtle but critical difference transforms how individuals can approach healthcare decisions with both wellness and financial efficiency in mind.

Even psychological health can play a role in qualifying for deductions. In rare but documented cases, individuals suffering from body dysmorphic disorder (BDD) or other diagnosed mental health conditions have pursued surgical interventions under psychiatric supervision. When such procedures are part of a treatment plan prescribed by licensed professionals, they may be considered medically necessary. The key is not the outcome — improved appearance — but the process: was the surgery recommended to alleviate a diagnosed condition? If so, the path to deductibility becomes clearer.

When “Elective” Becomes “Deductible” — Redefining the Rules

The word “elective” often carries a misleading connotation in financial and medical discussions. Many assume that if a procedure is optional — meaning not immediately life-threatening — it cannot be deductible. But the IRS does not categorize medical expenses by urgency alone. Instead, it focuses on whether the treatment serves a legitimate medical purpose. This means that even surgeries commonly associated with aesthetics can qualify as deductible if they address underlying health issues.

Take breast reduction surgery, for example. While some may view it as a cosmetic enhancement, thousands of women undergo the procedure to relieve chronic back, neck, and shoulder pain caused by overly large breasts. Medical records showing years of physical therapy, chiropractic visits, and persistent discomfort can support the argument that the surgery is functional, not frivolous. When physicians document conditions such as skeletal deformation, skin irritation, or postural problems directly linked to breast size, the IRS is more likely to accept the expense as valid.

Likewise, eyelid surgery (blepharoplasty) may be deductible when excess skin impairs vision. Patients who struggle to see clearly due to drooping eyelids can obtain visual field tests from ophthalmologists proving functional limitation. These objective results transform what might appear to be a vanity-driven choice into a vision-correcting medical necessity. The presence of measurable impairment makes all the difference.

Rhinoplasty, again, serves as another powerful example. While reshaping the nose for symmetry or proportion is non-deductible, correcting structural abnormalities that obstruct airflow falls squarely within acceptable medical grounds. Sleep apnea, recurrent nosebleeds, or difficulty exercising due to restricted breathing can all justify surgical intervention. In such cases, pulmonologists or ENT specialists may conduct breathing assessments, sleep studies, or endoscopic exams to provide clinical evidence. This medical validation shifts the classification from cosmetic to corrective — and from out-of-pocket to potentially tax-advantaged.

The takeaway is clear: it’s not the name of the surgery that determines deductibility, but the reason behind it. Taxpayers should not dismiss procedures simply because they alter appearance. What matters is whether a licensed healthcare provider has determined that the surgery addresses a diagnosable condition affecting physical or mental health. By reframing the conversation around medical necessity rather than societal perception, individuals gain access to financial tools they might otherwise overlook.

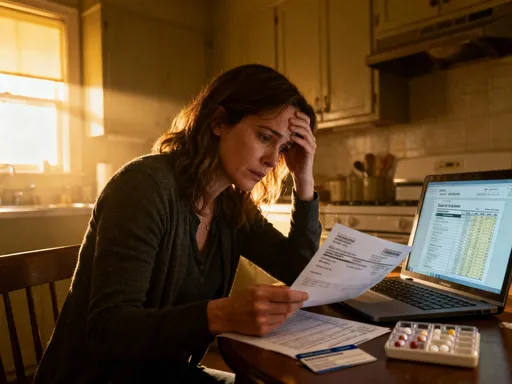

Building a Paper Trail That Works

No deduction survives scrutiny without solid documentation. Even the most legitimate medical expense can be denied during an audit if proper records are missing. For procedures straddling the line between cosmetic and medical, the burden of proof rests entirely on the taxpayer. This means creating a comprehensive, well-organized paper trail long before filing taxes — ideally from the moment the decision to pursue surgery is made.

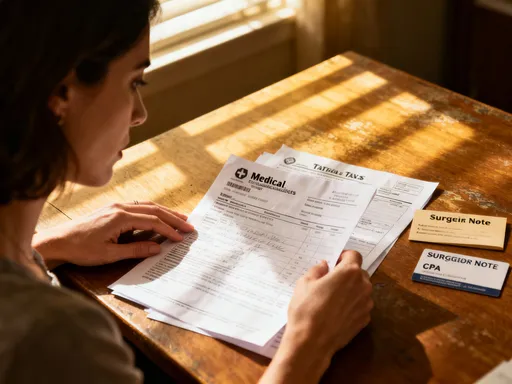

The foundation of any successful claim begins with a letter from the treating physician. This letter should clearly state the medical necessity of the procedure, referencing specific symptoms, diagnoses, and failed conservative treatments. It must avoid vague language and instead use precise clinical terms — such as “chronic musculoskeletal pain secondary to macromastia” rather than “patient wants smaller breasts.” The more detailed and objective the explanation, the stronger the case.

In addition to physician letters, patients should collect copies of all relevant medical records. These include diagnostic test results (like MRIs, X-rays, or pulmonary function tests), treatment plans, and progress notes from prior consultations. Diagnosis codes listed on insurance claims — known as ICD-10 codes — also serve as important validation. For instance, code M54.5 (low back pain) or R06.89 (other abnormalities of breathing) can reinforce the functional basis of a procedure. Itemized bills from the surgeon, anesthesiologist, and facility should also be preserved, showing exactly what services were rendered and their associated costs.

Communication with healthcare providers is essential in ensuring that documentation meets IRS standards. Many doctors are not familiar with tax requirements, so patients may need to request specific wording in letters or ask for additional testing to strengthen their case. For example, a patient seeking deduction for back pain relief after breast reduction might benefit from a referral to a physical therapist whose reports document posture improvement post-surgery. These follow-up records can demonstrate measurable outcomes, further validating the medical rationale.

Digital organization is equally important. Storing scanned copies of all documents in a secure, labeled folder — either on a personal drive or encrypted cloud storage — ensures easy retrieval if needed. A chronological timeline of events, from initial consultation to post-op checkups, helps present a coherent narrative. Some taxpayers even create a summary sheet listing each document type, date, and purpose, making it easier for accountants or auditors to verify the claim. Thoughtful preparation turns emotional healthcare experiences into structured, audit-ready financial strategies.

Timing Matters — Syncing Surgery with Tax Years

Strategic timing can significantly enhance the financial benefits of medical deductions. Because the IRS only allows deductions for medical expenses that exceed 7.5% of adjusted gross income (AGI), concentrating costs within a single tax year can make the difference between qualifying and missing out. This requires careful planning, especially for elective procedures that allow flexibility in scheduling.

Imagine a taxpayer with an AGI of $80,000. The threshold for deductibility would be $6,000 (7.5% of $80,000). If their annual medical expenses average $4,000, they fall short. But by moving forward a planned surgery — say, a $5,000 breast reduction for back pain — into the same year, total expenses rise to $9,000, exceeding the threshold by $3,000. That amount becomes deductible, reducing taxable income and potentially lowering their tax bill.

This bundling strategy works best when combined with other predictable medical costs. Dental work, prescription medications, vision corrections, or therapy sessions can all be scheduled in the same year to maximize the deduction. Even non-surgical treatments related to the same condition — such as physical therapy before or after surgery — count toward the total. The goal is not to incur unnecessary expenses, but to align existing or planned ones for optimal tax impact.

Flexible Spending Accounts (FSAs) and Health Savings Accounts (HSAs) add another layer of financial efficiency. Both allow individuals to pay for qualified medical expenses with pre-tax dollars, effectively reducing the net cost of surgery. An FSA, typically offered through employers, lets workers set aside up to a certain limit annually (adjusted for inflation), which must be used within the plan year or a short grace period. An HSA, available to those with high-deductible health plans, offers even greater advantages: contributions are tax-deductible, earnings grow tax-free, and withdrawals for medical purposes are untaxed. Using HSA funds to pay for a deductible surgery means paying with money that never faced income tax — a powerful compounding benefit.

However, coordination is crucial. Since taxpayers cannot double-dip — deducting expenses paid with pre-tax dollars — careful tracking is required. Expenses paid from an FSA or HSA are not eligible for itemized deductions. Therefore, it often makes sense to use pre-tax accounts for smaller, routine costs and reserve larger, qualifying expenses for itemization. Alternatively, some choose to pay out of pocket in a high-expense year, claim the deduction, and later reimburse themselves from an HSA — a strategy known as “HSA arbitrage” that leverages tax-free growth over time.

Working with Professionals — The Power of Team Strategy

Navigating the intersection of medicine and taxation is not a solo endeavor. Success depends on collaboration among multiple professionals — each bringing specialized expertise to the table. Physicians understand anatomy and pathology, accountants understand tax codes, and tax advisors understand compliance. Bridging these domains is where real financial value is created.

A primary care doctor or specialist may recommend a procedure for medical reasons but may not know how to phrase it for tax purposes. Conversely, a CPA may recognize the potential for a deduction but lack the medical knowledge to assess legitimacy. This gap can lead to missed opportunities or, worse, improper claims that trigger audits. To avoid this, patients should proactively facilitate communication between their healthcare providers and financial advisors.

One effective approach is to schedule a consultation with both the physician and the accountant present — either in person or via secure teleconference. During this meeting, the medical rationale can be explained in lay terms while ensuring that documentation aligns with IRS expectations. The accountant can guide the physician on what language strengthens the claim, such as emphasizing functional improvement over aesthetic change. This collaborative effort ensures that the paperwork supports both medical and financial objectives.

When assembling this team, it’s important to ask the right questions. For physicians: “Can you write a letter stating this procedure is medically necessary to treat a diagnosed condition?” For accountants: “Does this expense meet current IRS criteria for deduction?” For tax preparers: “Have you handled similar cases before? What documentation do you require?” These conversations build confidence and reduce the risk of errors.

Another common pitfall is inconsistency across records. If a patient tells their surgeon the surgery is for back pain but later describes it as “for confidence” on a tax form, red flags emerge. Uniformity in messaging — across medical files, insurance claims, and tax filings — is essential. A unified narrative, supported by consistent documentation, withstands scrutiny and demonstrates good faith.

Finally, working with professionals who specialize in medical tax planning can offer peace of mind. Some CPAs focus specifically on healthcare-related deductions and understand the nuances of IRS rulings. They may know about lesser-known provisions or recent case law that supports claims. While general practitioners can handle basic filings, specialized guidance increases the likelihood of approval — especially for complex or borderline cases.

Beyond the Deduction — Long-Term Financial Planning

Medical tax deductions are not isolated events; they are components of a broader financial strategy. When integrated wisely, they can influence long-term outcomes in retirement planning, investment eligibility, and overall tax positioning. Lowering taxable income through legitimate deductions can reduce tax brackets, increase eligibility for education credits, or improve qualification for income-based student loan repayment plans.

For example, a taxpayer in the 22% federal tax bracket who claims $4,000 in additional medical deductions saves $880 in federal taxes. That reduction in taxable income might also lower state taxes, depending on jurisdiction. Over time, repeated use of this strategy — especially for individuals managing chronic conditions requiring periodic interventions — compounds into meaningful savings.

Additionally, lower reported income can affect retirement account contributions. Some retirement plans, like Roth IRAs, have income limits that phase out at certain AGI thresholds. By reducing AGI through medical deductions, individuals may remain eligible to contribute to these accounts, preserving access to tax-free growth in retirement. Similarly, lower income can improve eligibility for premium tax credits under the Affordable Care Act, reducing health insurance costs in future years.

State-level variations also matter. While the federal government sets a 7.5% AGI threshold, some states have different rules. A few states do not allow itemized medical deductions at all, while others set higher or lower thresholds. Residents should consult local tax regulations to understand how their state treats these expenses. In states with no income tax, the federal benefit stands alone; in others, there may be additional savings.

The most effective financial planning views health spending not as a loss, but as an investment — one that yields both physical and monetary returns. By treating surgery costs as part of a holistic financial picture, individuals gain greater control over their economic future. This mindset shift — from passive spender to strategic planner — empowers smarter decisions across all areas of personal finance.

Real Stories, Real Savings — Lessons from Actual Cases

Theoretical knowledge gains power through real-world application. Consider the case of a middle school teacher in Ohio who suffered from chronic back pain due to large breasts. For years, she relied on painkillers, physical therapy, and custom-fitted bras. Her orthopedist documented progressive spinal curvature and recommended breast reduction surgery. After obtaining letters from both her primary physician and specialist, she scheduled the procedure in a year when she also underwent knee surgery. Combined, her medical expenses totaled $14,000 — well above the 7.5% AGI threshold. With proper documentation, she deducted over $8,000, saving nearly $2,000 in federal and state taxes.

Another example involves a construction worker in Colorado who lost part of his face in a workplace accident. Reconstructive surgeries over two years included skin grafts, orbital repair, and nasal reconstruction. Though emotionally taxing, each procedure was deemed medically necessary. His accountant helped him track every expense, from hospital stays to follow-up dermatology visits. By filing jointly with his spouse and itemizing deductions, they reduced their taxable income significantly, qualifying for a larger child tax credit the following year.

A third case features a collegiate track athlete from Virginia who struggled with severe snoring and daytime fatigue. A sleep study diagnosed obstructive sleep apnea, and an ENT specialist identified a deviated septum as the cause. After undergoing septoplasty, his breathing improved, and his athletic performance rebounded. Because the surgery was medically indicated, the family used HSA funds to pay the bill and later claimed related expenses — including the sleep study and CPAP machine — as part of a broader medical deduction. The combination of pre-tax spending and itemized deductions minimized their out-of-pocket burden.

These stories share common threads: preparation, persistence, and professional guidance. None involved loopholes or aggressive interpretations. Each individual worked within the system, followed the rules, and documented thoroughly. Their success was not accidental — it was the result of informed, ethical planning. They did not seek to exploit the tax code but to understand it and use it as intended.

What sets these cases apart is not the procedures themselves, but the mindset. These individuals approached healthcare decisions with both physical and financial well-being in mind. They asked questions, gathered evidence, and coordinated experts. In doing so, they turned personal challenges into opportunities for financial resilience.

Cosmetic surgery costs don’t have to be purely out-of-pocket burdens. With careful planning, the right documentation, and a strategic mindset, they can become part of a smarter financial journey. It’s not about gaming the system — it’s about understanding it. When health and finance align, you gain more than relief; you gain control. Every medical decision carries emotional weight, but when approached with foresight, it can also carry financial benefit. The tools are available, the rules are clear, and the outcomes are within reach — for those willing to learn, prepare, and act with integrity.