How I Survived My Worst Investment Loss — And What It Taught Me About Smart Cost Control

I once lost more than I thought possible in a market crash. It wasn’t just about the money — it was the stress, the sleepless nights, the regret. But that painful experience became my turning point. Instead of chasing quick wins, I shifted focus: not on what I could gain, but on what I could protect. This is how I rebuilt my strategy, centered on controlling costs and minimizing risk — not just surviving losses, but preparing for them. What began as a story of failure evolved into a lesson in resilience, discipline, and the quiet power of financial caution. For many women managing household finances, especially those balancing family needs with long-term goals, this shift in mindset can be life-changing.

The Day Everything Went Wrong

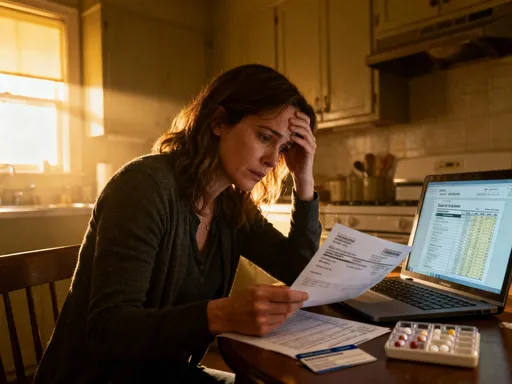

It started quietly — a few red numbers on a screen, nothing alarming at first. Then came the news: global markets were reacting to rising inflation and shifting central bank policies. Within days, what had been a steady climb in portfolio value reversed sharply. For someone who had built their investments over years through careful planning and reinvested dividends, the drop felt personal. One morning, a single glance at the account summary revealed a loss exceeding 30 percent in just three weeks. The shock was paralyzing. Sleep became difficult, and each new market update triggered anxiety. This wasn’t a speculative bet gone wrong; it was a portfolio designed for growth, diversified across sectors, and considered relatively safe. Yet, it still bled value rapidly.

What made the experience worse wasn’t just the financial hit, but the emotional toll. There was guilt — had I ignored warning signs? Had I trusted too much in past performance? There was fear — could this be the beginning of a longer downturn? And there was helplessness, watching decisions made years ago now unraveling without immediate control. The realization dawned that while growth had been the goal, protection had been an afterthought. Many investors, particularly those managing money for their families, operate under similar assumptions: that steady contributions and long-term holding are enough. But volatility doesn’t discriminate. It tests not just portfolio structure, but emotional resilience and preparedness.

This moment of crisis exposed a flaw in conventional investment thinking — the belief that time in the market guarantees safety. While historically true over decades, short-term disruptions can erode confidence and capital simultaneously. For women who often serve as financial anchors in their households, such losses carry added weight. They may delay retirement plans, affect children’s education funding, or strain marital budgets. The lesson wasn’t that investing is dangerous, but that relying solely on optimism is risky. A better approach was needed — one that acknowledged uncertainty and prioritized stability over spectacle.

Why Chasing Returns Backfires in a Crisis

Before the downturn, the focus had always been on returns. Which fund outperformed last quarter? Which stock delivered double-digit gains? These questions dominated conversations and influenced decisions. The pursuit of high returns felt logical — more growth meant faster progress toward goals. But during the crash, that mindset became a liability. As prices fell, the instinct was to act — to sell losing positions or chase emerging 'bargains.' Each move, driven by urgency rather than strategy, deepened the losses. This behavior is common and understandable, yet it contradicts sound financial principles. Chasing returns, especially in turbulent times, often leads to buying high and selling low — the exact opposite of successful investing.

The problem with return-focused thinking is that it ignores timing and context. Markets move in cycles, and periods of rapid growth are often followed by corrections. When investors fixate on recent performance, they tend to extrapolate trends into the future, assuming past winners will continue winning. This creates vulnerability. During downturns, the same assets once seen as reliable become sources of panic. Emotional reactions take over: fear triggers selling at lows, while greed resurfaces when markets rebound, leading to late entries at higher prices. This cycle repeats across generations, affecting both novice and experienced investors alike.

What’s missing is a counterbalance — a framework that values consistency over excitement. High returns are appealing, but they often come with elevated risk. When volatility strikes, those risks materialize quickly. A portfolio built for maximum growth may lack buffers, leaving little room for error. The shift needed isn’t away from growth entirely, but toward a more balanced perspective. Instead of asking, “How much can I earn?” the better question becomes, “How much can I afford to lose?” This subtle change in focus transforms decision-making. It encourages caution, promotes planning, and reduces the likelihood of impulsive moves. For women managing household finances, this approach offers peace of mind — knowing that even in crisis, the foundation remains intact.

The Hidden Power of Cost Control in Investing

One of the most overlooked aspects of investing is cost control. Most discussions center on returns, but costs silently erode wealth over time. After the market downturn, a closer look revealed that expenses — both visible and hidden — had been undermining performance long before prices dropped. These included management fees, trading commissions, tax inefficiencies, and behavioral costs like frequent buying and selling. While individually small, their cumulative effect was significant. Over ten years, even a 1% annual fee can reduce portfolio value by nearly 10%, compounding the damage during downturns.

Cost control is not about frugality; it’s about efficiency. Think of it as strengthening the foundation of a house. A well-built structure may not look impressive from the outside, but it withstands storms better. Similarly, a low-cost investment strategy doesn’t promise headline-grabbing gains, but it preserves more of what you earn. Consider index funds versus actively managed funds. The former typically charge lower fees because they track market benchmarks rather than relying on expensive research teams. Historically, many index funds have matched or outperformed their costlier counterparts over time, simply by keeping more of the market’s return.

Another hidden cost is taxes. Frequent trading in taxable accounts generates capital gains, which reduce net returns. By contrast, holding investments longer or using tax-advantaged accounts like IRAs or 401(k)s, investors can defer or minimize tax liabilities. Behavioral costs are equally important. The urge to react to market news often leads to unnecessary trades, each carrying fees and potential tax consequences. Over time, these actions chip away at compounding growth. Controlling these costs isn’t glamorous, but it’s powerful. For women who value stability and long-term security, focusing on what they can control — rather than chasing unpredictable returns — leads to better outcomes.

Building a Risk-Aware Investment Framework

After the losses, the priority shifted from performance tracking to risk management. The goal was no longer to beat the market, but to survive its worst moments with minimal damage. This required a new framework — one designed not for perfection, but for resilience. At its core was diversification, but not just across stocks and bonds. True diversification means spreading risk across asset classes, geographies, and investment styles. For example, combining U.S. equities with international exposure, real estate investment trusts, and fixed-income securities helps reduce reliance on any single market’s performance.

Asset allocation became the anchor of the strategy. Rather than adjusting holdings based on market sentiment, a fixed percentage was assigned to each category based on risk tolerance and time horizon. This allocation was reviewed annually, not daily, reducing the temptation to react impulsively. Position sizing also played a key role. No single investment was allowed to dominate the portfolio, limiting the impact of any one failure. These structural choices created a buffer — not a guarantee against loss, but a plan for managing it.

Equally important was defining personal risk limits. Before the crash, there was no clear threshold for when to reassess or exit a position. Now, loss limits were established — for example, a 15% decline in any holding would trigger a review, not an automatic sale. This provided a rule-based response instead of an emotional one. Additionally, emergency funds were strengthened to prevent forced selling during downturns. Knowing that living expenses were covered allowed for patience, letting investments recover naturally. This framework didn’t eliminate risk, but it made it measurable and manageable — a crucial shift for anyone seeking long-term financial well-being.

Cutting Costs Without Sacrificing Growth Potential

Reducing costs doesn’t mean abandoning growth. The objective is efficiency — achieving market-like returns while minimizing unnecessary expenses. One of the most effective steps was switching to low-cost investment vehicles. Exchange-traded funds (ETFs) and index mutual funds, known for their transparency and low expense ratios, replaced higher-fee alternatives. These funds still provided exposure to broad market gains, but with less drag on performance. Over time, the difference in net returns became noticeable, especially during flat or declining markets when every percentage point mattered.

Another area of optimization was transaction frequency. The old habit of adjusting the portfolio monthly or quarterly was replaced with a disciplined, long-term approach. Trades were made only when necessary — such as rebalancing once a year or adjusting allocations due to life changes. This reduced trading fees and tax implications while reinforcing commitment to the plan. Additionally, account types were evaluated for tax efficiency. Retirement accounts were used for less tax-efficient investments like bonds, while taxable accounts held equities with lower turnover. This strategic placement helped maximize after-tax returns.

Some might worry that cost-conscious investing means missing opportunities. But the data suggests otherwise. Most actively managed funds fail to beat their benchmarks over ten years, even before fees. By focusing on low-cost, broadly diversified options, investors position themselves to capture market returns without paying a premium for underperformance. For women managing family finances, this approach offers a practical balance — participating in growth while protecting capital. It’s not about getting rich quickly, but building wealth steadily and safely over time.

Tools and Habits That Keep Emotions in Check

Emotional discipline is one of the most valuable tools in investing, yet it’s rarely taught. After the crash, it became clear that structure was needed to prevent impulsive decisions. One effective habit was scheduling regular portfolio reviews — quarterly or semi-annually — rather than checking daily. This reduced exposure to short-term noise and created space for thoughtful evaluation. Market fluctuations still happened, but they no longer dictated actions.

Automated investing was another game-changer. Setting up automatic contributions to retirement and brokerage accounts ensured consistency, regardless of market conditions. This practice, known as dollar-cost averaging, naturally smoothed out purchase prices over time. Buying more shares when prices are low and fewer when high reduces the risk of mistiming the market. For busy women juggling work and family, automation also saved time and mental energy, making investing less stressful.

Journaling investment decisions added another layer of accountability. Before making any change, the reason was written down: Was it based on a long-term plan, or a reaction to news? Revisiting these notes later revealed patterns — how emotions influenced choices during volatile periods. This self-awareness improved decision-making over time. Together, these habits formed a system that supported rational behavior, even when markets were chaotic. They didn’t eliminate feelings, but they prevented those feelings from driving financial outcomes.

Turning Losses Into Long-Term Gains

Looking back, the worst investment loss became one of the most valuable lessons. It didn’t just change a portfolio — it changed a mindset. The obsession with returns gave way to a deeper understanding of financial health: sustainability, control, and peace of mind. True success in investing isn’t measured by peak performance, but by resilience through downturns. It’s about sleeping well at night, knowing that a plan exists for both growth and protection.

For women who manage household finances, this perspective is especially powerful. They often carry the responsibility of ensuring stability, planning for education, healthcare, and retirement. By focusing on cost control, risk management, and emotional discipline, they build not just wealth, but confidence. These principles don’t promise overnight riches, but they deliver something more lasting — the ability to weather storms and emerge stronger.

The journey from loss to wisdom wasn’t easy, but it was necessary. It taught that while markets are unpredictable, behavior doesn’t have to be. By controlling what can be controlled — expenses, exposure, and emotions — investors gain power over their financial futures. Preparedness replaces fear. Discipline replaces doubt. And resilience becomes the true measure of success. In the end, the greatest return isn’t on the portfolio statement — it’s in the quiet confidence that comes from knowing you’re ready, no matter what comes next.