How I Manage Money While Living with a Chronic Illness — An Expert’s Real Talk on Fund Control

Living with a chronic condition doesn’t just affect your health—it reshapes your entire financial life. I’ve been there: surprise bills, endless meds, and the stress of uncertain income. Over time, I learned how to protect my finances without sacrificing care. This is my real journey managing funds wisely, avoiding pitfalls, and staying financially resilient—all from an expert perspective who’s also living it daily. It’s not about getting rich or chasing high returns. It’s about creating stability when your body and income aren’t predictable. It’s about making sure that when flare-ups come, your bank account doesn’t break before your body does. This is the honest conversation many need but few have—one that blends lived experience with financial expertise to help you take control, even when life feels out of control.

The Hidden Financial Toll of Chronic Disease

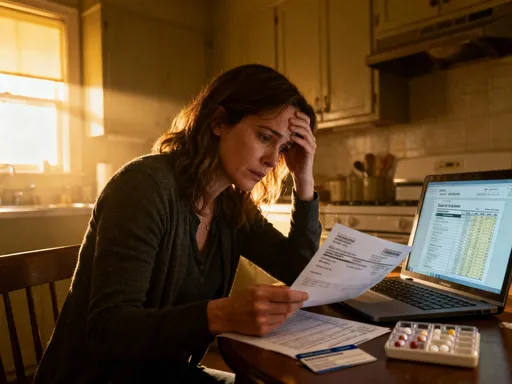

Chronic illness carries a financial burden that often goes unseen until it’s too late. While most people plan for emergencies like car repairs or home maintenance, few anticipate the long-term drain of managing a persistent health condition. Unlike acute medical events—such as a broken bone or short hospital stay—chronic diseases like diabetes, lupus, multiple sclerosis, or rheumatoid arthritis demand continuous care. This means ongoing expenses: monthly medications, regular specialist visits, diagnostic tests, physical therapy, and sometimes home modifications or mobility aids. These costs accumulate quietly, month after month, year after year, creating what economists call a “slow financial bleed.”

The impact isn’t limited to direct medical bills. Many individuals with chronic conditions experience reduced work capacity. Some transition to part-time roles, while others leave the workforce entirely due to fatigue, pain, or treatment schedules. This reduction in income creates a dual crisis: expenses rise while earnings fall. A study published in the journal Health Affairs found that individuals with chronic conditions spend, on average, 2.5 times more on healthcare annually than those without. When combined with lost wages, the total financial impact can exceed tens of thousands of dollars over a decade. These figures aren’t abstract—they represent real trade-offs: skipping social activities, delaying home repairs, or postponing retirement savings.

Another hidden cost is insurance complexity. Even with coverage, patients face deductibles, co-pays, and non-covered treatments. Insurance plans often exclude certain medications or require lengthy prior authorization processes, leading to out-of-pocket expenses that catch families off guard. Additionally, many chronic conditions require off-label or specialty drugs, which are frequently more expensive and less likely to be fully covered. This gap between expected and actual costs undermines traditional budgeting models, which assume medical spending is occasional rather than constant. As a result, families may deplete emergency savings within months of diagnosis, leaving them vulnerable to future shocks.

Emotional stress amplifies the financial strain. The anxiety of not knowing how much a treatment will cost—or whether it will be approved—can lead to avoidance behaviors. Some patients delay necessary care to avoid bills, worsening their condition and increasing long-term costs. Others make impulsive financial decisions, such as using high-interest credit cards to cover expenses, which creates cycles of debt. Recognizing this hidden toll is the first step toward building a financial strategy that acknowledges reality, not idealized assumptions. The goal isn’t to eliminate medical costs—those are often unavoidable—but to create a system that absorbs them without collapsing your financial foundation.

Why Standard Budgeting Falls Short—And What Works Better

Traditional budgeting methods, like the popular 50/30/20 rule—allocating 50% of income to needs, 30% to wants, and 20% to savings—assume financial stability. They work well for households with predictable incomes and steady expenses. But for someone managing a chronic illness, these models often fail. Energy levels fluctuate. Work hours vary. Medical needs shift from month to month. One month, a patient might have no unexpected costs; the next, they face a $1,200 infusion treatment or a last-minute specialist visit. Rigid budgets can’t adapt to this variability, leading to constant stress and frequent deviations.

A more effective approach is dynamic budgeting—flexible financial planning that adjusts to health cycles. Instead of setting fixed monthly categories, dynamic budgeting uses rolling forecasts based on current health status. For example, during a stable period with minimal symptoms, more funds can be directed toward savings or debt repayment. During a flare-up, the budget shifts to prioritize medical costs and essential living expenses. This method doesn’t abandon structure—it redefines it. It accepts unpredictability as a core variable and builds in mechanisms to respond without panic.

One practical way to implement dynamic budgeting is through a “health-phase” framework. Divide the year into anticipated phases: low-impact, moderate-impact, and high-impact periods. These can be based on past patterns, seasonal triggers, or treatment cycles. Assign budget ranges to each phase rather than fixed amounts. For instance, medication costs might range from $200 to $600 per month depending on the phase. This range becomes part of the financial plan, allowing for variation without surprise. It also helps identify when to draw from reserves or adjust non-essential spending.

Another key element is buffer integration. Standard budgets often include a single emergency fund for rare events. But for chronic illness, emergencies are frequent. A better model includes multiple buffers: a medical buffer, an income-gap buffer, and a general emergency buffer. These are small, designated pools of money that absorb shocks without disrupting the entire financial plan. For example, if a treatment costs $800 more than expected, the medical buffer covers it—no need to raid retirement savings or delay rent. These buffers are funded gradually, even during stable months, creating resilience over time. The shift is from rigid control to adaptive management—less about sticking to a plan, more about having the tools to adjust when life changes.

Building a Resilient Fund Structure: Protection First

Financial resilience begins with structure. When income and expenses are unpredictable, the way you organize your money becomes critical. A well-designed fund structure acts like a series of dams, preventing one financial overflow from flooding your entire life. Instead of a single checking account where everything mixes, consider separating funds into distinct categories, each with a specific purpose. This method, known as “fund compartmentalization,” reduces decision fatigue and protects long-term goals from short-term crises.

The first and most important fund is the medical reserve. This account is dedicated solely to healthcare-related expenses: prescriptions, co-pays, lab tests, and non-covered treatments. It should hold enough to cover three to six months of average medical costs. For someone spending $400 monthly on medications and visits, that means $1,200 to $2,400 set aside. This fund prevents medical bills from derailing other financial priorities. It also reduces stress—knowing there’s a designated pot of money for health needs makes decisions easier during flare-ups.

The second fund is for living essentials: housing, utilities, groceries, and transportation. This should be funded first from every paycheck, even before savings or debt payments. The goal is to ensure basic stability regardless of health status. Automating transfers to this account reinforces consistency. If income drops, this fund remains protected, preserving dignity and security. Many find it helpful to keep this money in a high-yield savings account linked to their primary checking, allowing easy access without temptation to overspend.

The third fund addresses income gaps. Chronic illness often leads to reduced work hours or temporary disability. An income-gap fund bridges the difference between actual earnings and essential expenses. It’s not meant to replace full income but to cover the shortfall. For example, if your rent is $1,200 and you earn $800 in a low-income month, the fund covers the $400 difference. Building this fund takes time—start with $50 per month and increase as possible. Over two years, even modest contributions can create a $1,200 to $2,000 cushion.

A fourth fund, if feasible, supports long-term goals like retirement or education. This is the last to be funded, only after protection-focused accounts are established. Contributions can be small—$25 to $50 monthly—but consistency matters more than size. The key is to start early, even with limited resources. Over time, compound growth turns small inputs into meaningful outcomes. This structured approach doesn’t eliminate financial challenges, but it transforms them from crises into manageable variations. It gives control back to the individual, turning uncertainty into a navigable path rather than a cliff edge.

Smarter Investing When Health Is Unpredictable

Investing with a chronic illness requires a different mindset. Traditional advice often emphasizes long-term growth, assuming investors can ride out market downturns over decades. But when your income is unstable and medical needs are immediate, liquidity and stability become just as important as returns. The goal isn’t to maximize gains—it’s to preserve capital while allowing for modest growth that outpaces inflation without exposing funds to excessive risk.

Low-volatility investment strategies are ideal in this context. These include index funds that track broad markets, dividend-paying stocks from established companies, and bond funds with strong credit ratings. These assets tend to fluctuate less than speculative stocks or cryptocurrencies, reducing the chance of losing money when you might need to access it. For example, a diversified portfolio of 60% bonds and 40% equities has historically provided steady returns with lower risk than an all-stock portfolio. This balance allows for growth while protecting against sudden drops.

Liquidity is another critical factor. Some investments, like real estate or retirement accounts with early withdrawal penalties, are hard to access quickly. For someone with a chronic condition, having part of the portfolio in liquid assets—such as money market funds or short-term CDs—ensures that funds are available when needed. A common rule is to keep 6 to 12 months of essential expenses in easily accessible accounts. This isn’t part of the emergency fund per se, but a separate component of the investment strategy that prioritizes flexibility.

Asset allocation should reflect personal health timelines. If you expect frequent medical expenses in the next five years, aggressive investments may not be appropriate. Instead, focus on capital preservation. As health stabilizes and time horizon extends, you can gradually shift toward growth-oriented assets. This personalized approach ensures that investment choices align with real-life needs, not generic advice. It also reduces stress—knowing your portfolio won’t force you to sell low during a market dip or health crisis.

Professional guidance can help tailor these decisions. A fee-only financial advisor with experience in chronic illness planning can assess risk tolerance, time horizons, and liquidity needs to build a customized strategy. The cost of advice should be weighed against the value of peace of mind and better outcomes. Investing isn’t about getting rich—it’s about ensuring that the money you’ve worked hard to save continues to serve you, even when your body doesn’t cooperate.

Cutting Costs Without Compromising Care

Saving money while managing a chronic illness doesn’t mean cutting corners on treatment. It means being strategic about where and how you spend. Many patients unknowingly pay more than necessary for medications, supplies, and services. With a few informed choices, it’s possible to reduce out-of-pocket costs significantly without sacrificing quality of care.

One of the most effective tools is patient assistance programs. Many pharmaceutical companies offer discounts or free medications to eligible patients based on income and insurance status. These programs are underutilized, often because patients don’t know they exist or assume they won’t qualify. Applying takes time—documentation is required—but the savings can be substantial. For example, a monthly medication that costs $600 out-of-pocket might be available for $0 through a manufacturer’s program. Resources like NeedyMeds.org and the Partnership for Prescription Assistance provide searchable databases to find these opportunities.

Pharmacy pricing varies widely, even for the same drug. Using price-comparison tools like GoodRx or SingleCare can reveal savings of 50% or more at different pharmacies. Some insurance plans even allow mail-order prescriptions at lower co-pays. Additionally, choosing generic versions when available—after consulting with a doctor—can reduce costs without affecting efficacy. These small actions, repeated monthly, add up to hundreds or even thousands in annual savings.

Preventive care is another cost-saving strategy. Regular check-ups, screenings, and vaccinations can catch complications early, avoiding expensive treatments later. Many insurance plans cover preventive services at no cost—yet patients skip them due to time or transportation issues. Addressing these barriers, such as scheduling telehealth visits or arranging ride-sharing, pays long-term dividends.

Non-medical changes can also support both health and budget. Remote work setups reduce commuting costs and energy expenditure. Energy-efficient home modifications—like better insulation or LED lighting—lower utility bills and improve comfort for those sensitive to temperature. Even dietary shifts, such as planning meals in advance or buying in bulk, can reduce grocery spending while supporting better health. The goal is to align financial decisions with wellness, creating a system where saving money also means feeling better.

Navigating Insurance and Government Support Wisely

Understanding insurance and public benefits is one of the most powerful financial skills for someone with a chronic illness. Yet, the system is complex, filled with jargon and bureaucratic hurdles. Many patients miss out on available support simply because they don’t know how to navigate it. Taking time to understand your benefits can lead to significant savings and income protection.

Start with your health insurance. Know the difference between deductibles, co-pays, and co-insurance. Understand what your plan covers—and what it doesn’t. Request a detailed summary of benefits from your provider. If a treatment is denied, don’t accept it immediately. You have the right to appeal. Many denials are overturned with proper documentation from your doctor. Keep records of all medical bills, prescriptions, and correspondence. Organize them in a dedicated folder, digital or physical. This makes appeals faster and more effective.

Disability benefits are another critical resource. Social Security Disability Insurance (SSDI) and Supplemental Security Income (SSI) provide monthly payments to those unable to work due to medical conditions. The application process is lengthy and requires extensive medical evidence, but approval can stabilize income for years. Working with a disability attorney or advocate increases the chances of success, especially during appeals.

Tax advantages are often overlooked. Certain medical expenses can be deducted if they exceed a percentage of your adjusted gross income. Contributions to Health Savings Accounts (HSAs) are tax-deductible and can be used for qualified medical costs. If you have a high-deductible health plan, an HSA is a powerful tool for saving pre-tax dollars for future care.

Coordination is key. Avoid accidentally exceeding income limits for programs like Medicaid by understanding how different benefits interact. In some cases, earning slightly more can lead to losing benefits, creating a “welfare cliff.” Planning with a benefits counselor helps avoid these pitfalls. Knowledge isn’t just power—it’s financial protection.

Long-Term Financial Confidence: Planning Beyond Today

Living with a chronic illness doesn’t mean abandoning long-term financial goals. Retirement, legacy planning, and personal autonomy are still within reach—even if the path looks different. The key is consistency, not perfection. Small, regular actions build resilience over time, creating a foundation that supports both present needs and future dreams.

Retirement planning remains essential. Even if you can’t contribute large amounts, starting early with whatever you can afford makes a difference. IRAs and employer-sponsored plans allow for catch-up contributions later. The goal isn’t to match others’ savings—it’s to ensure you have options as you age. A financial advisor familiar with chronic illness can help project income needs and adjust strategies accordingly.

Legacy considerations, such as wills or advance directives, provide peace of mind. They ensure your wishes are respected and reduce burden on loved ones. These documents don’t have to be complex. Many legal aid organizations offer free or low-cost assistance with basic estate planning.

Maintaining autonomy is perhaps the most valuable outcome. Financial control means fewer decisions are dictated by crisis. It means choosing treatments based on medical need, not cost alone. It means having the freedom to rest when needed, without guilt or fear. This level of confidence doesn’t come overnight. It comes from setting up systems, learning your rights, and making informed choices—one step at a time.

The journey of managing money with a chronic illness is ongoing. There will be setbacks and surprises. But with the right structure, mindset, and support, financial stability is achievable. It’s not about perfection—it’s about progress. And progress, no matter how small, builds a future where health challenges don’t define your financial destiny.