How I Finally Got Smart About Timing My Experience Spending

Remember that feeling when you splurge on a concert, trip, or fancy dinner and wonder—was it worth it? I’ve been there, over and over. As a beginner navigating experience consumption, I kept missing the sweet spot between enjoyment and financial sense. It wasn’t until I started treating these moments like smart investments—timing them right—that everything changed. This is how I learned to get more joy without the regret. What began as a series of small, seemingly harmless indulgences gradually revealed a pattern: the timing of my spending often dictated not just the cost, but the depth of satisfaction. The lesson wasn’t about cutting back—it was about choosing wisely, waiting strategically, and aligning each experience with both my emotional readiness and financial stability. That shift made all the difference.

The Hidden Cost of Impulse Experiences

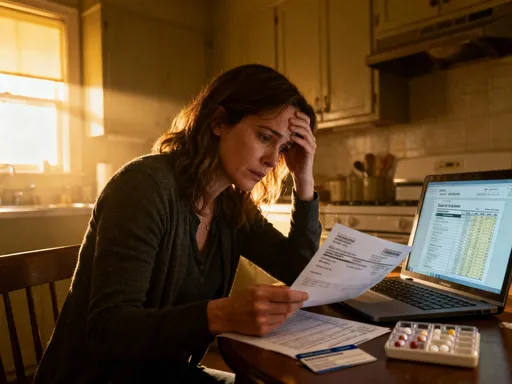

Many people treat experiences as exceptions to their budget, something to be justified rather than planned. A last-minute weekend getaway, a spontaneous concert ticket, or a sudden reservation at a trendy restaurant—these moments often feel exciting in the moment but can carry hidden financial and emotional costs. The real issue isn’t the expense itself, but the lack of intention behind it. When decisions are driven by impulse, the aftermath frequently includes not just a lighter wallet, but a sense of regret. This regret isn’t always about money alone; it’s the realization that the timing was off, the need was reactive, and the joy was fleeting.

Impulse experiences are often rooted in emotional triggers. Stress, loneliness, or the fear of missing out—commonly known as FOMO—can push individuals toward spending that feels good in the short term but undermines long-term financial confidence. Social media amplifies this by constantly showcasing curated highlights of other people’s lives, creating a false sense of urgency to keep up. A friend posts a photo from a tropical beach, and suddenly, a vacation feels essential—even if the savings account is already stretched thin. These external pressures cloud judgment, making it harder to distinguish between genuine desire and emotional reaction.

What changes this pattern is a shift in mindset: viewing experiences not as spontaneous treats, but as intentional investments in well-being. When you begin to assess not just *what* you’re spending on, but *why* and *when*, the decision-making process becomes more deliberate. This doesn’t mean eliminating fun or denying yourself pleasure. Instead, it means ensuring that the pleasure lasts longer than the transaction. A well-timed experience, entered into with clarity and readiness, tends to leave a deeper, more lasting impression. The key is recognizing that timing isn’t just logistical—it’s psychological and financial.

Moreover, poorly timed spending can disrupt cash flow in ways that ripple through other areas of life. Using credit to fund an unplanned trip may mean delaying a necessary car repair or dipping into an emergency fund. These trade-offs often go unnoticed in the moment but contribute to long-term financial stress. By contrast, when experiences are aligned with periods of financial stability—such as after receiving a bonus or during a low-spend month—the impact is far less disruptive. The same experience, enjoyed under different financial conditions, can feel either like a burden or a celebration. That difference is largely a matter of timing.

Why Timing Matters More Than the Experience Itself

It’s easy to assume that the quality of an experience depends entirely on the event—the destination, the performer, the restaurant. But research in behavioral finance and psychology suggests otherwise. The *timing* of an experience significantly influences how much we enjoy it and whether we view it as worthwhile. A vacation taken during a period of high stress may leave you exhausted rather than refreshed. A concert enjoyed while worrying about unpaid bills can feel hollow, no matter how talented the artist. The context in which we consume experiences shapes our perception of their value.

Consider the concept of “peak-end rule,” a principle in behavioral economics that suggests people judge experiences largely based on how they felt at their peak and at their end. If a trip begins with flight delays and ends with a lost suitcase, the memory may be dominated by frustration—even if the days in between were enjoyable. Timing, therefore, affects not just the immediate moment but the lasting impression. Booking an experience during a period of personal calm and financial ease increases the likelihood that both the peak and the end will be positive, enhancing overall satisfaction.

External factors also play a crucial role. Seasonal demand, for example, directly impacts both cost and experience quality. A ski trip booked during peak holiday weeks will be more expensive and more crowded than the same trip taken two weeks later. The slopes, the lodges, the restaurants—all are more congested, reducing the sense of relaxation and escape. By shifting the timing even slightly, travelers can access better rates and a more peaceful environment. The same principle applies to concerts, festivals, and dining reservations. Off-peak timing often means not just savings, but a superior experience.

Personal cash flow patterns are equally important. Most households have predictable rhythms—certain months are tighter, others more generous. Aligning experience spending with high-cash-flow periods, such as after tax refunds or annual bonuses, allows for greater comfort and less financial strain. This doesn’t require complex budgeting; it simply involves awareness. When you time your spending to coincide with natural surpluses, the experience feels like a reward rather than a risk. And because there’s no lingering financial pressure, the enjoyment is purer, more complete.

Furthermore, economic cycles can influence the value of experiences. During periods of lower inflation or reduced travel demand, prices for flights, accommodations, and event tickets may be more favorable. While no one can predict the economy with perfect accuracy, staying informed about broader trends—such as airline pricing patterns or event industry forecasts—can help identify windows of opportunity. These moments don’t last forever, but they do recur. Recognizing them allows for smarter, more strategic decisions that maximize both affordability and satisfaction.

Spotting the Signals: When to Spend and When to Wait

Smart timing isn’t about rigid rules or endless waiting—it’s about learning to read the signals that indicate whether a decision is strategic or reactive. These signals fall into three main categories: personal financial rhythms, external economic conditions, and emotional readiness. By tuning into each, individuals can make more informed choices about when to move forward and when to pause.

First, personal financial rhythms offer a reliable internal compass. Most people have predictable cycles of income and spending. Some months are naturally lean—perhaps due to annual insurance payments or back-to-school expenses—while others bring extra income, such as holiday bonuses or tax refunds. Tracking these patterns over time reveals optimal windows for experience spending. For example, planning a family outing in a high-income month reduces the need to rely on credit or dip into savings. This kind of alignment doesn’t require drastic lifestyle changes; it simply involves matching desires with financial reality.

Second, external economic indicators can provide valuable context. Airfare prices, for instance, tend to follow seasonal trends, with lower rates available during shoulder seasons—periods just before or after peak travel times. Event ticket pricing often reflects demand cycles, with early-bird rates offering significant savings. Subscribing to price alerts or using fare comparison tools can help identify these opportunities without constant monitoring. The goal isn’t to chase the absolute lowest price, but to avoid paying a premium due to poor timing. Even a few weeks’ difference in booking can result in substantial savings.

Third, emotional readiness is often the most overlooked signal. Are you considering a trip because you genuinely want to, or because you’re trying to escape stress? Is a dinner reservation driven by celebration, or by a need to prove something to yourself or others? Emotional clarity helps distinguish between meaningful experiences and impulsive reactions. A simple pause—such as a 48-hour waiting period before confirming a purchase—can create space for reflection. During that time, many people realize that the initial urge was temporary, fueled by mood rather than intention.

Real-life examples illustrate the power of these signals. One woman delayed a solo retreat after recognizing that her motivation was burnout, not curiosity. When she finally went six months later—after a period of rest and financial preparation—she described the experience as transformative, rather than exhausting. Another individual waited to book concert tickets until after receiving a work bonus, allowing him to enjoy the event without financial anxiety. In both cases, the experience was the same, but the timing made the difference between regret and fulfillment.

Turning Experiences into Value-Driven Investments

Experiences don’t appear on a balance sheet, but they can deliver lasting returns in ways that go beyond money. When timed well, they contribute to emotional well-being, strengthen relationships, and even support personal or professional growth. Reframing experiences as value-driven investments shifts the focus from cost to impact. Instead of asking, “How much did this cost?” the more useful question becomes, “What did this give me?”

Consider a networking dinner. On the surface, it may seem like a simple meal with colleagues. But when timed around a career transition or a new professional goal, it can open doors to mentorship, collaboration, or job opportunities. The financial cost is modest, but the potential return—measured in confidence, connections, or career advancement—is significant. Similarly, a well-planned solo trip can provide space for reflection, creativity, and personal clarity. These outcomes aren’t incidental; they’re outcomes of intentional timing.

Even seemingly small experiences can accumulate long-term value. A monthly coffee date with a close friend may appear minor, but over time, it strengthens emotional support systems, which are crucial during challenging periods. A family outing to a local museum or park may seem like simple entertainment, but it builds shared memories and reinforces bonds. When these moments are timed to coincide with periods of connection—rather than conflict or distraction—their impact deepens.

The key is alignment. An experience that aligns with a current life goal—whether it’s improving mental health, strengthening relationships, or advancing a career—feels more meaningful and justified. It ceases to be a guilty pleasure and becomes a deliberate step forward. This doesn’t mean every outing must have a purpose, but that the most satisfying ones often do. By asking, “Does this support where I am right now?” individuals can make choices that feel both enjoyable and intentional.

Moreover, value-driven experiences tend to generate positive ripple effects. A relaxing weekend getaway can recharge energy, leading to greater productivity at work. A cultural event can spark new interests or conversations that enrich daily life. These benefits aren’t always immediate, but they contribute to a sense of well-being that compounds over time. When experiences are treated as investments in quality of life, the return isn’t measured in dollars, but in resilience, joy, and connection.

Building a Simple Framework for Smarter Decisions

Turning insight into action requires a practical approach. A simple, three-step framework can help anyone make more thoughtful decisions about experience spending. The method is designed to be accessible, requiring no special tools or financial expertise—just awareness and consistency.

The first step is to pause and assess emotional state. Before making any booking or reservation, take a moment to reflect: Am I feeling pressured, stressed, or impulsive? Or am I calm, clear, and genuinely excited? Emotions are valid, but they shouldn’t be the sole driver of financial decisions. A brief pause—such as the 48-hour rule—creates space to distinguish between fleeting urges and lasting desires. This small delay often reveals whether the motivation is internal or external, emotional or intentional.

The second step is to evaluate timing against cash flow and external factors. Is this a high-spend or low-spend month? Is income stable right now? Are there upcoming bills that could create strain? At the same time, consider broader conditions: Are prices favorable? Is this peak or off-peak season? This step doesn’t require perfect information—just a basic awareness of financial and market rhythms. Even a quick mental check can prevent costly missteps.

The third step is to reflect on alignment with personal goals. Does this experience support a current priority—such as rest, connection, or growth? Will it contribute to long-term well-being, or is it primarily about short-term escape? This reflection grounds the decision in values rather than impulses. It transforms spending from a reaction into a choice.

To reinforce this framework, small habits can make a big difference. Keeping a “joy journal” to record past experiences—what was enjoyed, what wasn’t, and why—provides valuable feedback over time. Reviewing these entries helps identify patterns in what truly brings satisfaction. Another helpful habit is setting intention-based budgets—allocating funds not just for categories like “travel” or “dining,” but for purposes like “reconnection” or “renewal.” This adds meaning to the numbers and makes spending feel more purposeful.

Common Traps and How to Avoid Them

Even with good intentions, people fall into predictable traps that undermine smart timing. One of the most common is chasing trends—booking a popular restaurant or attending a viral event simply because others are doing it. While social connection is valuable, following the crowd without reflection can lead to spending that feels hollow afterward. The experience may be enjoyable, but if it doesn’t align with personal preferences or current needs, the satisfaction is often short-lived.

Another trap is overcompensating for stress. After a difficult week, the urge to “treat” oneself can feel justified. But if the treat is used as a temporary escape rather than a planned recovery, it may provide momentary relief but deepen long-term stress. A luxury weekend booked in emotional exhaustion may leave behind not just memories, but credit card debt and guilt. The solution isn’t denial, but preparation. Scheduling rest and enjoyment in advance—as part of a balanced routine—ensures that these moments are restorative, not reactive.

Trying to impress others is another distortion of timing. Upgrading a reservation or choosing a more expensive option to appear successful can lead to financial strain and inauthentic experiences. The goal shifts from personal enjoyment to external validation, which rarely brings lasting satisfaction. Recognizing personal “warning signs”—such as feeling the need to document everything for social media—can help identify when motives are shifting.

To avoid these traps, it helps to set clear intentions before engaging in any experience spending. Asking simple questions—“Am I doing this for me?” or “Would I still want this if no one else knew?”—can restore focus. Additionally, creating a personal “decision filter” based on values, goals, and financial limits makes it easier to say no without guilt. The aim isn’t perfection, but progress—a gradual shift toward more mindful, more satisfying choices.

From Spender to Strategist: A Mindset Shift

Mastery of timing transforms not just spending habits, but one’s entire relationship with money. When experiences are no longer seen as indulgences to be justified, but as intentional choices to be planned, confidence grows. The fear of regret diminishes, replaced by a sense of control and clarity. This isn’t about waiting indefinitely or denying pleasure—it’s about arriving at the right moment, fully present and free from financial anxiety.

Each decision becomes an opportunity to practice mindfulness and discipline. Over time, the pattern of pausing, assessing, and aligning becomes second nature. The result is not just better experiences, but a deeper sense of financial well-being. Money is no longer a source of stress, but a tool for creating a meaningful life. The joy of a well-timed dinner, a thoughtfully planned trip, or a quiet afternoon with a book becomes richer because it is chosen, not stumbled into.

Smart timing is not about sacrifice. It’s about alignment—between desire and readiness, between spending and values, between momentary pleasure and lasting satisfaction. It’s about understanding that the best moments are not always the most spontaneous, but the most intentional. And when you learn to time your experiences with care, you don’t just spend money wisely—you live more fully.