How I Balanced My Car Loan and Built Wealth Without Stress

Buying a car often feels like a win—until the loan payments start piling up. I was overwhelmed too, juggling monthly bills while trying to save. But what if your car loan didn’t drain your finances, but actually helped shape smarter money habits? It all started with one idea: asset allocation isn’t just for investors. By treating my car as part of my financial picture, not a standalone expense, I found a way to pay less, save more, and avoid common money traps.

The Hidden Cost of Car Loans: More Than Just Monthly Payments

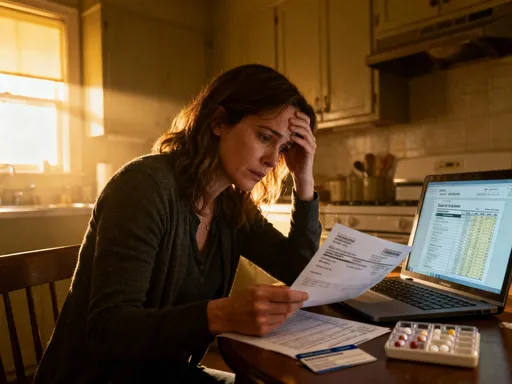

When most people consider a car loan, they focus on the monthly payment and interest rate. While these are important, they represent only a fraction of the true financial impact. The real cost of a car loan extends beyond the contract—it affects your cash flow, credit utilization, and long-term ability to respond to life’s surprises. A $400 monthly payment may seem manageable on paper, but when it consumes 20% of your take-home pay, it can silently crowd out opportunities to build emergency savings, invest, or even handle unexpected medical or home repair costs.

One of the most overlooked aspects is how car loans influence your debt-to-income ratio, a key factor lenders examine when you apply for a mortgage or personal loan. Even if you make every payment on time, carrying a large auto loan can reduce your borrowing power in the future. This becomes especially critical for families planning major life events like buying a home or funding education. The psychological burden is real, too—knowing that a significant portion of each paycheck is already spoken for can create a sense of financial rigidity, making it harder to feel in control.

Another hidden cost is depreciation. Unlike a home or investment, a car loses value the moment it leaves the lot—often 20% in the first year alone. This means you’re not just paying interest on borrowed money; you’re also losing equity over time. Many buyers end up underwater on their loans, owing more than the car is worth, especially if they make a small down payment or finance for longer than five years. This imbalance increases financial risk if the car is damaged or needs to be sold unexpectedly.

Yet another layer is insurance and maintenance. These ongoing costs are frequently underestimated. Full coverage insurance for a financed vehicle is typically required by lenders and can add $100 or more per month. Routine maintenance, tire replacements, and repairs further strain the budget. Over five years, these expenses can add thousands to the total cost of ownership. Without planning, they can turn a manageable payment into a source of constant stress.

The key insight is that a car loan isn’t an isolated financial decision—it’s a recurring claim on future income. It shapes what you can do with your money for years. Recognizing this shifts the mindset from simply qualifying for a loan to evaluating whether the purchase aligns with broader financial goals. Awareness is the first step toward control. Once you see the full picture, you can make intentional choices that protect your financial flexibility and set the stage for smarter money management.

Why Asset Allocation Matters Even with Debt

Many people believe asset allocation is a strategy reserved for investors with portfolios of stocks and bonds. In reality, asset allocation is simply about how you divide your financial resources among different needs and goals—and it applies to everyone, regardless of income level or debt status. Even if you’re paying off a car loan, deciding how much to allocate to debt repayment, emergency savings, and future growth is a form of asset allocation. The goal is balance: ensuring that one financial obligation doesn’t dominate at the expense of long-term stability.

One common mistake is the all-or-nothing approach—either paying the minimum on the car loan and saving nothing, or throwing every extra dollar at the debt and leaving no buffer for emergencies. Both extremes carry risks. The first leaves you vulnerable to setbacks; the second can lead to burnout and missed opportunities. A smarter path is to treat your finances like a diversified portfolio, where each category serves a purpose. Debt reduction protects your credit and frees up future cash flow. Savings provide security. Small investments, even in low-risk instruments like high-yield savings accounts or retirement funds, begin the process of compounding growth.

Consider this: if you have a car loan at 5% interest and also maintain a high-yield savings account earning 4%, the math may suggest paying off the loan first. But emotionally and practically, having even a small emergency fund can prevent you from relying on credit cards when a tire blows or the transmission fails. That protection often outweighs the slight interest differential. The psychological benefit of knowing you’re not one surprise away from debt spiraling is invaluable.

Moreover, consistent saving—even in small amounts—builds financial discipline. Automating a $50 monthly transfer to a savings account reinforces the habit of paying yourself first. Over time, these contributions grow, and the account becomes a tool for opportunity, not just survival. When a bonus or tax refund arrives, having a clear allocation strategy helps you decide whether to apply it to the loan, boost savings, or do both.

The misconception that you must be debt-free before investing is widespread but flawed. Delaying savings until debt is gone can cost you years of compound growth. Starting early, even with modest amounts, leverages time—the most powerful force in wealth building. The key is proportionality. If your car loan payment is 15% of your income, aim to allocate at least 10% to savings and debt combined, adjusting based on your timeline and goals. Asset allocation with debt isn’t about perfection; it’s about progress and balance.

Mapping Your Financial Ecosystem: Where the Car Loan Fits In

To manage a car loan effectively, you need to see it within the context of your entire financial life. Think of your finances as an ecosystem—every element is connected, and changes in one area affect the whole. Income flows in, expenses flow out, and goals guide the direction. Without a clear map, it’s easy to misplace priorities or underestimate trade-offs. But when you visualize your financial picture, the car loan stops being a standalone burden and becomes a manageable part of a larger system.

Start by listing your monthly income after taxes. Then, categorize your expenses into fixed (rent, utilities, insurance, loan payments) and variable (groceries, dining, entertainment, gas). Include the car loan in fixed costs, but also account for variable car-related expenses like fuel, maintenance, and parking. This gives a complete picture of transportation costs, which many people underestimate. Next, identify your financial goals—short-term (emergency fund), mid-term (vacation, home down payment), and long-term (retirement, education).

With this map, you can assess whether your current spending aligns with your priorities. For example, if your transportation costs consume 25% of your income, that may leave little room for savings or other goals. This doesn’t mean you must sell your car, but it does mean you may need to adjust elsewhere—perhaps by reducing dining out, refinancing the loan, or carpooling to save on gas. The goal is not austerity, but alignment.

One practical tool is the 50/30/20 guideline: 50% of income for needs, 30% for wants, and 20% for savings and debt repayment. If your car loan pushes needs over 50%, you’ll need to compensate by adjusting wants or increasing income. This framework helps you make conscious trade-offs. For instance, choosing a slightly older car with a lower payment might free up $150 per month—enough to fund a retirement contribution or build a cushion in savings.

Another benefit of mapping your finances is spotting inefficiencies. Maybe you’re paying for premium insurance you no longer need, or your phone bill is higher than market rates. Small savings in one area can create space for better debt management or goal progress. The process also builds awareness of cash flow timing—knowing when bills are due helps avoid late fees and overdraft charges, which add hidden costs to an already tight budget.

Over time, this financial map becomes a living document. Review it quarterly or after major life changes. As your income grows or expenses shift, your allocations can evolve. The car loan will eventually end, but the habit of mapping your finances equips you to handle future decisions—like buying a home or planning for retirement—with greater confidence and clarity.

The Payoff: Balancing Aggressive Repayment and Smart Saving

One of the most common financial dilemmas is whether to prioritize paying off a car loan quickly or building savings first. On one hand, eliminating debt brings peace of mind and frees up future income. On the other, having no savings leaves you vulnerable to setbacks that could lead to more debt. The answer isn’t either/or—it’s balance. A “minimum-plus” repayment strategy, combined with consistent saving, offers a sustainable path forward.

Minimum-plus means paying slightly more than the required monthly payment—perhaps an extra $50 or $100—while still funding essential savings. This approach accelerates debt payoff without sacrificing liquidity. For example, if your loan has a 5% interest rate and a $400 minimum payment, adding $100 per month could shorten the loan term by over a year and save hundreds in interest. At the same time, setting aside $50 monthly in a high-yield savings account builds a buffer that can cover unexpected repairs or job interruptions.

The emotional benefit of this strategy is significant. Aggressive repayment without savings can feel like walking a tightrope—any slip leads to disaster. But when you have even a modest emergency fund, you gain confidence. You’re no longer afraid of a flat tire or oil change derailing your progress. This reduces stress and makes it easier to stick with your plan over time.

Consider a real-life scenario: Sarah had a $25,000 car loan at 4.8% interest over five years. Instead of putting a $2,000 tax refund entirely toward the loan, she split it—$1,000 to the loan and $1,000 to savings. The extra payment reduced her loan term by eight months. The savings covered a $600 transmission repair six months later, preventing her from using a credit card. In the long run, she saved more in interest and avoided high-cost debt.

Another advantage of balance is flexibility. Life changes—job loss, family needs, medical issues—can happen at any time. If all your extra money goes to debt, you may have no choice but to borrow when emergencies arise. But if you’ve built even a three-month emergency fund, you can handle most setbacks without derailing your financial plan. The goal isn’t to eliminate all risk, but to manage it wisely.

Ultimately, financial progress is about momentum, not perfection. Paying a little extra on your loan while saving consistently builds both discipline and resilience. Over time, these small actions compound—debt shrinks, savings grow, and confidence increases. The payoff isn’t just a paid-off car; it’s the knowledge that you can manage money well, even under pressure.

Avoiding the Debt-to-Debt Trap: Building Financial Boundaries

One of the greatest risks of car ownership is falling into the debt-to-debt cycle—paying off one loan only to take on another, often with little improvement in financial position. This pattern is especially common when buyers trade in a paid-off car for a new financed vehicle, believing they’re upgrading when they’re actually resetting the clock on debt. Without clear boundaries, this cycle can continue for decades, delaying true financial freedom.

The root cause is often a lack of long-term planning. People focus on monthly payments rather than total cost or asset value. A $350 payment may seem affordable, but over six years, it totals more than $25,000—far exceeding the car’s resale value. When the loan ends, the car may be worth only half of what was paid, forcing the owner to finance the difference on the next vehicle. This “negative equity roll-in” is a major driver of perpetual debt.

To break the cycle, set clear financial boundaries. First, avoid financing a car for longer than five years. The longer the term, the more interest you pay and the greater the risk of being underwater. Second, make a down payment of at least 20% to build initial equity. Third, resist the temptation to buy new. A one- or two-year-old certified pre-owned vehicle can save thousands while offering similar reliability.

Another critical boundary is preparing for maintenance. Once the warranty expires, repair costs rise. Setting aside $50–$100 per month in a dedicated auto maintenance fund prevents surprises from becoming financial emergencies. This habit also reinforces the idea that a car is a depreciating asset—not an investment—and should be managed accordingly.

Finally, delay the next purchase as long as possible. Once your loan is paid off, keep driving the car. Use the former payment amount to boost savings or pay down other debts. This “snowball effect” accelerates financial progress. Over time, you’ll build a habit of conscious spending, where major purchases are planned, not impulsive. By treating the car as a tool, not a status symbol, you make decisions based on value, not emotion.

Small Shifts, Big Impact: Practical Habits That Support Both Goals

Lasting financial change doesn’t come from dramatic overhauls but from consistent, small habits. These behaviors, when practiced regularly, compound into meaningful progress. They require minimal effort but deliver maximum results over time. For anyone managing a car loan while building wealth, integrating a few key habits can make the difference between stress and control.

One of the most powerful is tracking net worth monthly. This simple act—listing all assets (savings, retirement accounts, home equity) and subtracting all liabilities (loans, credit cards)—provides a clear picture of financial health. Watching the number grow, even slowly, reinforces positive behavior. It also highlights the impact of extra loan payments or new savings, making progress tangible.

Another habit is automating small transfers. Set up automatic $25–$50 transfers from checking to savings or retirement accounts on payday. Because the money moves before you see it, spending isn’t affected. Over a year, this adds up to hundreds or even thousands saved—without feeling deprived. Automation removes willpower from the equation, making consistency easier.

Reviewing loan terms annually is another smart practice. Interest rates change, and your credit score may have improved since you financed the car. Refinancing could lower your rate and monthly payment, freeing up cash for other goals. Even a 1% reduction on a $20,000 loan can save hundreds over the remaining term. This habit ensures you’re not overpaying due to outdated terms.

Finally, practice mindful spending. Before any non-essential purchase, pause and ask: “Does this align with my goals?” This isn’t about denial—it’s about intention. Choosing to delay a $200 shopping trip to instead put $100 toward the loan and $100 into savings strengthens financial discipline. Over time, these choices build confidence and reduce impulse spending.

The key is sustainability. You don’t need to do everything at once. Pick one habit, master it, then add another. These small shifts, when repeated, create a foundation for long-term wealth. They turn financial management from a chore into a quiet source of pride.

Looking Ahead: From Car Loan to Financial Confidence

The journey of managing a car loan wisely is about more than just paying off a vehicle—it’s about building skills that apply to every financial decision. The discipline of budgeting, the foresight to save, the courage to make trade-offs—these are the habits of financial confidence. And confidence, more than any single investment or savings account, is the true foundation of wealth.

As the loan balance shrinks and savings grow, you begin to see money differently. It’s no longer just something that comes and goes; it’s a tool you can shape and direct. You learn that progress is possible, even with debt. You discover that small, consistent actions lead to real results. This mindset shift is powerful—it changes how you approach future goals, from buying a home to planning for retirement.

The end of the car loan isn’t the finish line; it’s a milestone. What matters most is the habits you’ve built and the awareness you’ve gained. You now know how to balance competing priorities, avoid common traps, and make decisions based on long-term value. These skills will serve you for decades.

Financial confidence doesn’t come from quick fixes or windfalls. It comes from showing up, month after month, making thoughtful choices. It comes from knowing you can handle life’s surprises without falling apart. And it comes from treating every dollar—not as a source of stress, but as an opportunity to build the life you want.

So if you’re in the middle of a car loan, feeling the pressure of monthly payments, remember this: you’re not just paying for a car. You’re investing in your financial future. Every payment, every saved dollar, every smart choice is building something greater. And that’s a journey worth taking.