How I Survived a Career Gap Without Going Broke — Real Financial Moves That Worked

Facing a sudden career break, I panicked—bills piled up, savings drained, and my confidence hit rock bottom. But instead of giving in, I took control. Through real strategies like emergency budgeting, smart side hustles, and risk-aware investing, I stabilized my finances. This isn’t a theoretical guide—it’s my raw, tested journey through one of life’s toughest financial tests. I didn’t have a safety net from wealth or family support. I was an ordinary professional, one missed paycheck away from crisis. What saved me wasn’t luck, but a series of deliberate choices grounded in financial discipline and emotional resilience. If you’re in the same boat, you’re not alone. And more importantly, you can survive this—and even emerge stronger.

The Breaking Point: When My Career Gap Hit

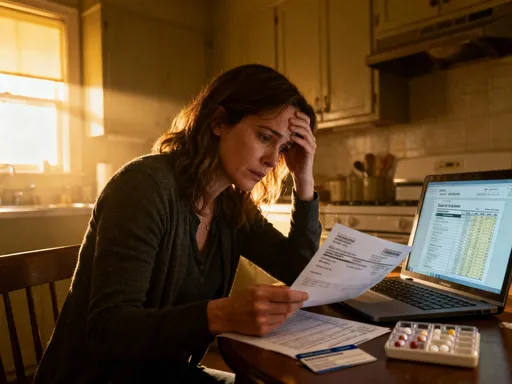

The call came on a Tuesday afternoon. A restructuring meant my position was being eliminated. Severance was offered, but it wouldn’t last beyond four months. At first, I tried to stay optimistic. I updated my resume, reached out to contacts, and applied to roles daily. But weeks passed with no offers. Then came the creeping anxiety: the rent due date loomed, the grocery bill felt heavier, and my savings account balance dropped with alarming speed. What began as a temporary pause quickly turned into a full-blown financial crisis. I wasn’t alone—career gaps affect millions, whether due to layoffs, caregiving responsibilities, health issues, or industry shifts. According to labor statistics, nearly one in four workers experiences an involuntary job loss before age 50. The emotional toll is often matched by the financial strain. I remember staring at my bank statement one night, calculating how many weeks I could stretch my money. The fear wasn’t just about money—it was about identity, stability, and control. I had always defined myself by my career. Without it, I felt invisible. But that moment of crisis also became a turning point. I realized that while I couldn’t control the job market, I could control my response. That clarity led me to the first essential step: creating an emergency financial plan from scratch.

What I learned in those early weeks was that financial survival isn’t about drastic measures—it’s about immediate, realistic adjustments. I stopped treating my situation as a short-term setback and began planning for a longer journey. I acknowledged that job searching could take months, not weeks. I also recognized that maintaining my previous lifestyle was no longer sustainable. This wasn’t failure—it was adaptation. I began tracking every expense, no matter how small. I reviewed recurring charges, from streaming services to insurance premiums. I contacted lenders and service providers to inquire about hardship programs. Many were willing to offer temporary relief, but I had to ask. The key was action, not paralysis. I also reached out to a financial counselor through a nonprofit credit advisory service. That conversation helped me see my finances clearly, without shame or judgment. It wasn’t about blame—it was about solutions. That shift in mindset—from panic to problem-solving—was the foundation of my recovery. The career gap didn’t disappear, but my ability to navigate it began to grow.

Emergency Budgeting: Cutting Back Without Losing Dignity

Once the shock wore off, I knew I needed a new budget—one built for survival, not comfort. I started by categorizing expenses into three groups: essentials, negotiables, and luxuries. Essentials included rent, utilities, groceries, and minimum debt payments. Negotiables were things like internet, phone, and insurance—necessary but adjustable. Luxuries were everything else: dining out, entertainment, subscriptions. I didn’t eliminate joy entirely, but I redefined it. A $5 coffee became a home-brewed cup. A night out turned into a movie at home. The goal wasn’t deprivation but sustainability. I used a simple spreadsheet to map out my monthly income and expenses. With no salary, my income came from severance, occasional freelance work, and a small emergency fund. I allocated funds strictly, giving each dollar a job. This method, often called zero-based budgeting, ensured nothing was wasted. I also built in a small discretionary line—$25 a week—for personal spending. This helped me avoid feeling restricted, which in turn made the budget easier to stick to.

One of the most effective changes was switching to a lower-cost grocery strategy. I began meal planning, buying in bulk when possible, and using store brands instead of name brands. I discovered that my local supermarket offered a discount day for seniors, but the policy allowed anyone to participate. I started shopping on those days and saved nearly 20% on my bill. I also used cash-back apps and loyalty programs, stacking small savings into meaningful reductions. Another major cut came from subscriptions. I reviewed every recurring charge and canceled those I didn’t actively use. That included a meditation app I hadn’t opened in months, a cloud storage plan I could downgrade, and a magazine subscription delivered digitally. I saved over $60 a month—enough to cover a utility bill. I also negotiated my internet and phone bills. A simple phone call to customer service, asking for retention offers, reduced my combined monthly cost by 30%. These weren’t dramatic moves, but together, they created breathing room. I learned that budgeting isn’t about shame—it’s about empowerment. Every dollar saved was a step toward stability.

Equally important was the mental shift. I stopped viewing budgeting as a punishment and began seeing it as financial self-defense. I reminded myself that this wasn’t permanent—it was a phase. I also avoided comparing my situation to others. Social media made it easy to feel inadequate, seeing former colleagues post about promotions or vacations. But I focused on my own progress. I celebrated small wins: a lower grocery bill, a successful negotiation, a week without overspending. I kept a journal to track my emotional state alongside my finances. This helped me recognize patterns—like how stress led to impulse spending—and adjust accordingly. I also leaned on free resources. Libraries offered not just books but free events, Wi-Fi, and even resume workshops. Community centers provided low-cost fitness classes. I found ways to maintain dignity while living frugally. The goal wasn’t to live poorly—it was to live wisely. And in that wisdom, I found strength.

Cash Flow Fixes: Side Gigs That Actually Pay Off

Budgeting helped me stretch my savings, but I needed income. Relying solely on severance wasn’t sustainable. I began exploring side gigs that could generate cash without requiring a major time investment. My background was in marketing, so I started with freelance writing and social media management. I signed up for reputable platforms where clients posted jobs, and I tailored my profile to highlight relevant experience. My first few gigs paid modestly—$50 here, $100 there—but they built momentum. I treated each project professionally, delivering on time and asking for testimonials. Positive feedback helped me win higher-paying work. Within two months, I was earning a few hundred dollars a month consistently. It wasn’t a salary, but it covered groceries and helped me avoid dipping into long-term savings.

I also explored gig economy options. I did weekend deliveries using a popular app, which required only a car and a few hours a week. The pay wasn’t high, but it was immediate and flexible. I scheduled deliveries during times when job searching was slow, turning idle hours into income. I also offered virtual assistant services to small business owners—handling emails, scheduling, and data entry. These tasks didn’t require deep expertise, but they saved clients time. I charged a flat rate per project, which made billing simple. Another source of income came from selling unused items. I decluttered my home and listed clothes, electronics, and furniture online. Platforms made it easy to photograph, price, and ship items. I earned over $1,200 in three months—money I funneled directly into my emergency fund. I avoided get-rich-quick schemes and anything that required an upfront payment. I knew those were often scams targeting people in financial distress.

Time management was crucial. I created a weekly schedule that balanced job searching, side work, and personal time. I used a digital calendar to block out hours for each activity. I treated side gigs like part-time jobs—consistent but not overwhelming. I also set income goals: first $200 a month, then $500, then $800. Each milestone felt like progress. I learned that side income doesn’t have to be glamorous to be valuable. What mattered was reliability and sustainability. I also discovered hidden skills. I’d always enjoyed organizing events, so I began offering virtual event planning for small gatherings. A friend referred me to a client, and that led to two more. These opportunities didn’t replace my career, but they kept me engaged and financially afloat. Most importantly, they restored a sense of agency. I wasn’t just waiting for a job—I was creating value. That mindset shift was as important as the money itself.

Protecting What’s Left: Risk Control in Uncertain Times

One of the biggest dangers during a career gap is making emotional financial decisions. Fear can lead to rash moves—like cashing out retirement accounts, investing in high-risk schemes, or taking on expensive debt. I saw others do it. A former colleague withdrew from his 401(k) to cover rent, only to face early withdrawal penalties and tax consequences. Another invested in a “guaranteed return” opportunity that turned out to be a scam. I made it a rule: no major financial decisions under stress. If a choice felt urgent, I waited 48 hours. That pause often revealed better options. I also reminded myself that preserving capital was more important than growing it during this phase. My goal wasn’t to get rich—it was to survive without permanent damage.

I reviewed my investment portfolio and decided to take a conservative stance. I avoided speculative stocks, cryptocurrency, and leveraged products. Instead, I focused on stability. I shifted a portion of my funds into low-volatility assets like bond funds and high-yield savings accounts. I didn’t try to time the market—I accepted that some fluctuations were normal. I also diversified what I could, spreading risk across asset classes. This wasn’t about maximizing returns; it was about minimizing losses. I stayed informed but didn’t obsess over daily market news. I checked my accounts once a week, not daily. This reduced anxiety and prevented emotional reactions. I also avoided borrowing unless absolutely necessary. When my car needed repairs, I considered a personal loan but ultimately used savings. It hurt to deplete that buffer, but it was better than adding debt with interest.

Mental resilience played a key role in risk control. I practiced mindfulness and routine to maintain emotional balance. A consistent sleep schedule, daily walks, and regular check-ins with supportive friends helped me stay grounded. I also limited exposure to financial fear-mongering content. Some media outlets thrive on panic, but I chose sources that offered balanced, factual reporting. I reminded myself that financial recovery is a marathon, not a sprint. Patience was a form of discipline. I also revisited my long-term goals regularly. Seeing a future beyond the gap helped me resist short-term temptations. I wrote down my values: security, independence, peace of mind. Every financial decision was measured against them. This clarity made it easier to say no to risky options. Protecting what I had wasn’t passive—it was an active, daily choice. And that choice became a source of strength.

Smarter Saving: Building a Buffer from Scratch

Even with low income, I made saving a priority. I started small—$10 a week, transferred automatically to a separate savings account. It felt symbolic at first, but consistency turned it into a habit. I used a digital bank with no fees and higher interest rates, which helped my balance grow slightly over time. I also set up micro-transfers: whenever I earned money from a side gig, 10% went straight into savings before I touched the rest. This “pay yourself first” approach ensured I didn’t spend everything. I also created a windfall rule: any unexpected money—like a tax refund or gift—went entirely into savings. One year, I received a small stimulus payment. Instead of spending it, I added it to my emergency fund. Over time, these small actions compounded. Within 18 months, I had rebuilt a $3,000 buffer—enough to cover a few months of essentials.

The psychological impact was profound. Saving, even a little, restored a sense of control. It signaled that I was moving forward, not just surviving. I also reframed saving as an act of self-respect. Every dollar set aside was a vote of confidence in my future. I avoided the trap of thinking “I’ll start when I earn more.” That mindset delays action. Instead, I believed that building the habit mattered more than the amount. I tracked my progress monthly and celebrated milestones. Reaching $500 felt like an achievement. Hitting $1,000 was a turning point. I shared these wins with a trusted friend, which reinforced accountability. I also used visual tools—a chart on my fridge showing my savings growth. It reminded me daily that progress was possible.

I learned that saving isn’t just about money—it’s about behavior. Automating transfers removed willpower from the equation. I didn’t have to decide each week; the system worked for me. I also avoided dipping into savings for non-emergencies. I defined what counted as an emergency: unexpected medical costs, essential home repairs, job search expenses. A sale on clothes didn’t qualify. This discipline protected my progress. I also reviewed my savings goals quarterly. As my income changed, I adjusted my targets. When I landed a part-time role, I increased my savings rate to 15%. The goal wasn’t perfection—it was consistency. And over time, consistency became confidence. I wasn’t just rebuilding a fund—I was rebuilding my financial identity.

Investing with Caution: Growing Value Without Gambling

Once my emergency fund was stable, I began thinking about long-term growth. Investing during a career gap felt counterintuitive—why risk money when I needed it most? But I realized that avoiding investing entirely could cost me in the long run. Inflation erodes cash value, so keeping all savings in a checking account wasn’t safe. The key was caution. I focused on low-cost, diversified options that required minimal effort. I chose index funds that tracked broad market performance, such as total stock market and international funds. These offered exposure to hundreds of companies with a single investment. I also used a robo-advisor, which automated portfolio allocation based on my risk tolerance and goals. It rebalanced regularly and kept fees low—under 0.25% annually.

I adopted dollar-cost averaging: investing a fixed amount each month, regardless of market conditions. This reduced the risk of buying at a peak. I started with $50 a month—affordable even on a tight budget. Over time, this strategy smoothed out volatility and built a position gradually. I didn’t try to predict market movements. I accepted that short-term fluctuations were normal and focused on long-term trends. I also educated myself through reputable sources—government financial literacy sites, university publications, and books by certified financial planners. I avoided sensationalized content that promised quick riches. I learned that successful investing isn’t about genius—it’s about consistency, patience, and low costs.

Importantly, I only invested money I wouldn’t need for at least five years. This ensured I could ride out downturns without panic. I kept my emergency fund separate and untouched. I also avoided leveraging or borrowing to invest. That kind of risk wasn’t worth it. My goal wasn’t to double my money—it was to preserve and grow it steadily. Over two years, my portfolio gained modestly, but more importantly, I gained confidence. I understood my investments, felt in control, and avoided emotional decisions. Investing became a tool for empowerment, not anxiety. It reminded me that financial health isn’t just about survival—it’s about building a future.

The Comeback: Returning Stronger Than Before

After 14 months, I landed a new role—part-time at first, then full-time. The job search was grueling, but my financial discipline had kept me afloat. More than that, it had transformed me. I returned to work with better habits, clearer priorities, and deeper resilience. I no longer took income for granted. I budgeted with intention, saved automatically, and invested with caution. I also brought new skills to the table—freelance experience, project management, and digital tools I’d learned during the gap. Employers valued that adaptability. I didn’t hide the career break—I framed it as a period of growth and reinvention.

The experience reshaped my relationship with money. I no longer saw it as a measure of worth, but as a tool for freedom. I had proven I could survive uncertainty without collapsing. That knowledge gave me peace. I also became more compassionate toward others facing financial challenges. I mentored a colleague going through a layoff, sharing budgeting tips and job search strategies. Giving back felt meaningful. I realized that setbacks don’t define us—our response does. The career gap didn’t break me; it rebuilt me. I emerged not just financially stable, but financially wiser. I had faced one of life’s toughest tests and learned that with discipline, patience, and practical action, it’s possible to survive—and even thrive.